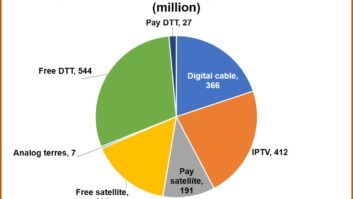

Global pay-TV penetration (the number of pay-TV subscriptions relative to the number of households) will see its first-ever yearly decline in 2024, according to research by Ampere Analysis.

The drop will follow pay-TV penetration peaking at 60.3 per cent in Q4 2023, says the analysts, who predict that by 2028, global pay-TV penetration will have fallen by almost four percentage points.

In North America, pay TV penetration has almost halved from a high of 84 per cent in 2009 to 45 per cent in 2023, said Ampere, adding that this has been caused by a combination of high costs and competition from a mature Subscription Video on Demand (SVoD) market.

Despite this decline, the annual revenue generated per user will sit at over $1,100 in 2023 across North America, the highest across any region, said the analysts.

Europe has seen the highest penetration growth in recent years, driven by low-cost IPTV services, which are often bundled into broadband packages for a low or nominal cost, reported Ampere. While these regions will also fall into decline after 2025, there are still some growth markets, such as Portugal, Serbia, and Hungary which are expected to see further growth in the forecast period.

Rory Gooderick, senior analyst at Ampere Analysis said: “Growth in global pay-TV uptake has been driven over the last five years by Asia Pacific and Central and Eastern Europe. However, declines coming from the Americas, which are driven by streaming competition and the high price of pay TV in North America, currently sitting at over $90 a month, will contribute to global pay TV penetration declining for the first time in 2024.

“Despite the projected decline in the reach of pay-TV products, cable and satellite platforms will remain a powerful force in the TV world, and important distribution partners for streaming products. This package structure, already increasingly common in Europe and parts of Asia, offers a framework for traditional cable TV companies to transition their business into a streaming aggregation play, and stabilise subscriber trajectories.”