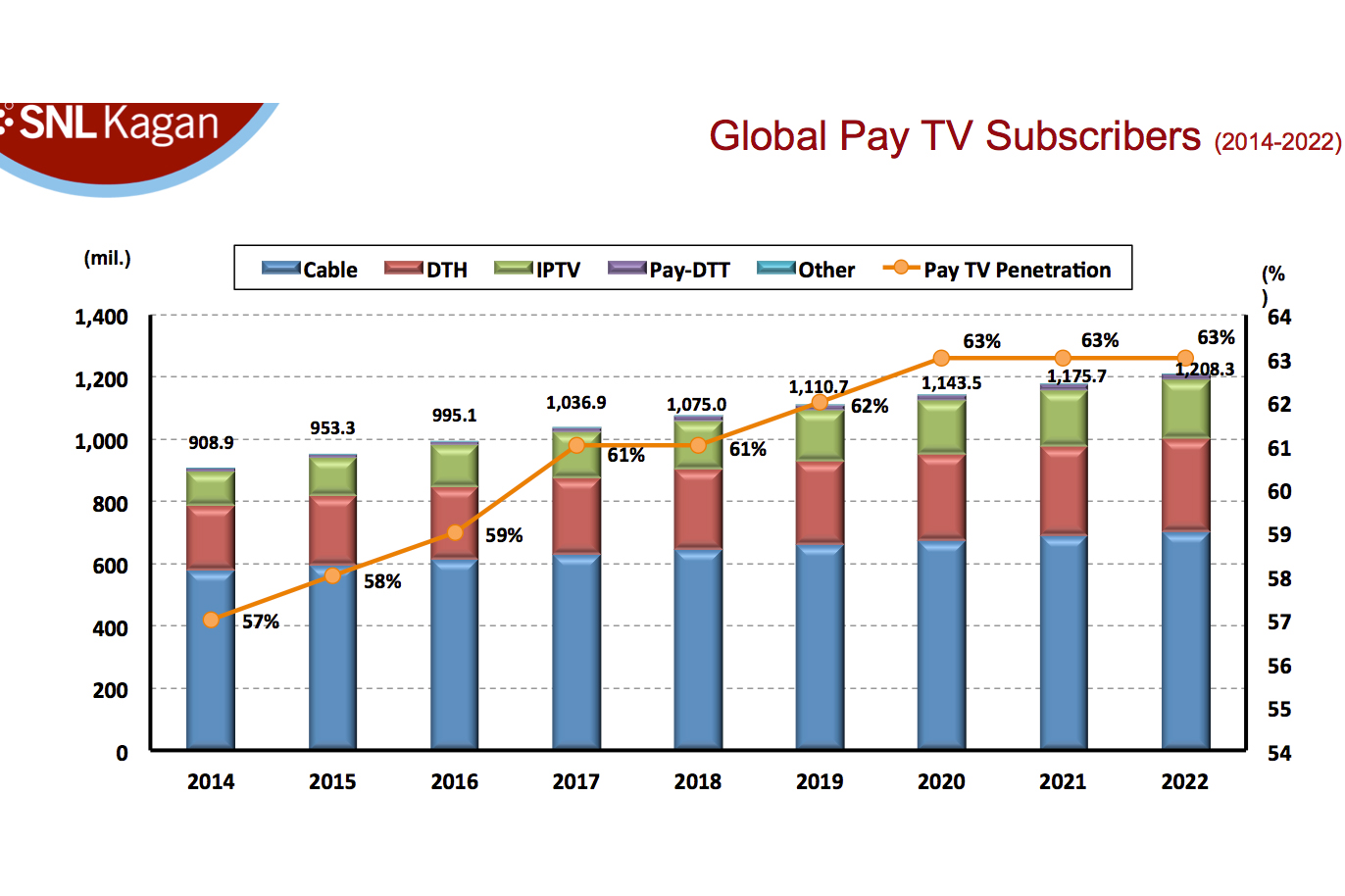

The global pay-TV market is projected to grow from more than 900 million subscribers in 2014 to 1.21 billion by 2022, while Europe will likely comprise 117.2 million subs by that year, according to SNL Kagan data.

Asia should contribute the largest number of global subs in 2022, as it did in 2014, while cable TV is expected to continue to serve more subscribers than either direct-to-home or IPTV worldwide, although the latter two platforms will continue to experience significant growth over the coming years.

We estimate that there were more than 582 million cable TV subs globally at year-end 2014, dwarfing the 207 million DTH subs and 109 million IPTV subscribers. Some of the largest cable TV/IPTV operators are in China — including the largest of any kind, the IPTV operator China Telecom with more than 29 million subs. Comcast Corp. in the US is the world’s largest cable operator with 22.4 million subs as of 31 March. The US is also home to the largest DTH provider in the world, DIRECTV, with 20.4 million subs as of the end of March, with Dish TV India taking the number two spot at more than 15.8 million subscribers. North America has the highest pay TV penetration regionally, followed by Eastern Europe and Asia.

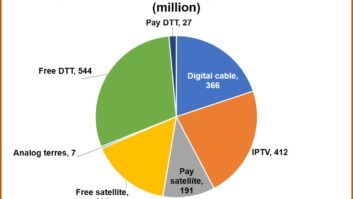

Multichannel subscribers in Western Europe are currently projected to grow from 108.1 million in 2014 to 117.2 million by 2022. The greatest expansion will come in IPTV services, thanks to the continued investment and development by telcos such as Orange in France, British Telecom in the UK and Spain’s Telefonica. Subscribers served by cable MSOs are expected to decline slightly over this time period as a result of increased competition from other multichannel operators — IPTV and DTH — as well as the growth of online video alternatives taking share in some markets.

However, operators across Europe are responding to streaming competition with the expansion of TV Everywhere and over-the- top services of their own. For example, Sky’s Now TV and Modern Times Group’s Viaplay are keeping customers within those companies’ suite of products even if those customers opt for only the streaming services. Operators across Europe such as the UK’s Virgin Media, France’s Numericable–SFR, Germany’s Deutsche Telekom AG, Denmark’s Waoo! and Sweden’s Com Hem have integrated Netflix into their set- top boxes. There is a notable overlap between Netflix subs and other OTT services as well as pay-TV services in some markets across Europe, with Sky TV, for example, reporting that around 40 per cent of Now TV subs also take Netflix and 20 per cent take Amazon.com’s Prime Instant Video.

Our data shows that broadband households exceed multichannel households in the leading markets of France, Germany and the UK, with the growing gap a focus for pay-TV operators. The aggressive rollout of triple- and quad-play services in France has limited the difference, but the gap is expected to increase over time. Aggressive bundling also now characterises the UK market, with BT and TalkTalk Telecom Group rolling out innovative bundles to compete with Virgin Media, which has achieved 90 per cent penetration of its triple/quad-play homes. In fact, in the UK there are few signs of cord cutting, with ample room still existing for pay-TV growth.

Cable and DTH operators in the UK market are achieving a growing penetration of connected devices, which is driving revenue growth from new products and services. Cable still has the competitive edge with high-speed broadband, while DTH provider and market pay-TV leader Sky targets a broad reach of services and premium exclusive content, with a big investment in originals. IPTV players TalkTalk and BT have been focusing in part on alleviating price pressure via bundles to gain market share, and they have achieved some success in selling smaller TV bouquets.

By Robin Flynn, senior analyst and research director, and Mohammed Hamza, TV and video analyst, SNL Kagan

This exclusive article is based on Robin Flynn’s presentation at this year’s TVBEurope2020 Breakfast Briefing